If you’ve ever walked into a bank and been told you “qualify for less house than last year,” you’ve felt purchasing power in action. In real estate, purchasing power is the amount of property your income, savings, and credit can actually buy after factoring in price, interest rates, and inflation. It’s the bridge between what homes cost and what people can pay—and it decides who gets in, who gets pushed out, and where markets boom or stall.

1) What purchasing power means in real estate

Definition: Within economics, buying power is the amount of money a person or group has available to spend on goods and services. In housing, it’s specifically ‘how much house your income and credit will buy after lenders run the numbers.

How it’s measured:

1. JLL Home Purchase Affordability Index (HPAI): Ratio of average household income to the ‘eligible income’ needed for a loan on a 1,000 sq ft apartment at market price.

– 100 = exactly enough income to qualify.

->100= surplus income; <100 = can’t qualify.

2. NAR Affordability Index: Measures if a median-income family can qualify for a mortgage on a median-priced home, assuming 20% down and payment ≤25% of income.

3. IMF Housing Affordability Index: Ability of a median-income household to qualify for a mortgage to buy an average-priced home, factoring price, income, rates, LTV, and term.

Core drivers: Income, house price, interest rate, down payment, and inflation. Change any one and purchasing power shifts immediately.

2) Why purchasing power matters

A. It sets real estate prices

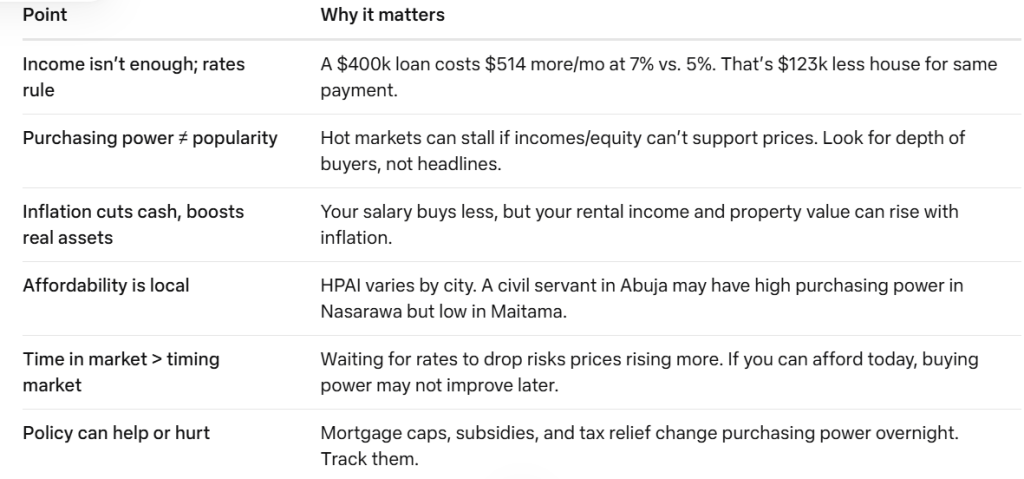

Buyer purchasing power is the driving force behind real estate pricing. Each mortgage-dependent buyer has a maximum price: down payment + mortgage funds they qualify for. When purchasing power falls, prices follow 9-12 months later due to “sticky” sellers. When it rises, prices rise ~6 months later.

Interest rates are the lever. A half-point rate move changes mortgage principal by tens of thousands. Example: $400,000 loan at 5% = ~$2,147/mo. At 7% = ~$2,661/mo. That’s $500+ more without a bigger house. A 1% rate increase can cut buying power by 10%+. In 2022, when rates jumped 3%→6%, a $2,500/mo budget lost $117,750 in buying power—from $517,500 to $399,750.

B. It determines affordability & inequality

Nearly 3/4 of experts polled by Reuters said housing would be less affordable in 2-3 years as prices rise and rates move higher. Younger buyers without equity are hit hardest: “for those without significant amounts of equity, prices have…moved ahead of them”.

House price growth has outpaced property tax revenues since 1995 because values rise faster than incomes and assessments. That gap fuels inequality.

C. It drives market cycles

Popular markets can stall when price growth outruns purchasing power. Popularity increases fast via media and investors, but purchasing power—income + equity—changes slowly. If prices rise faster than buyer capacity, growth stalls or depends on new buyers replacing old ones.

D. It’s an inflation hedge for assets, a tax on income

Real assets behave differently from bonds in inflation. Apartment rents adjust annually to market; replacement cost rises with materials/labor. That provides a floor under value and income that grows with inflation, while fixed-income loses real value.

3) When purchasing power comes into play

4) How it benefits investors

1. Inflation resistance = real returns. Rents and replacement costs rise with inflation. Unlike a 3% bond in 5% inflation, apartments can re-price annually.

2. Pricing power in scarce sectors. Industrial, retail, and residential with strong demand can raise rents, offsetting inflation drag.

3. Uncorrelated stability. Real assets have low correlation to public equities, stabilizing portfolios.

4. Timing advantage. When purchasing power falls broadly, cash buyers and investors with equity outbid first-time buyers. People with saved pandemic cash outbid those without.

5. Selectivity pays. Properties with strong demand + flexibility to raise rents maintain value. Those without see values erode.

Risk: Higher rates cut buying power for leveraged buyers. In 2022, Raleigh saw affordable homes drop from 61.1% to 33.2% as rates went 3%→6%. Already-expensive markets like Bay Area saw little change—affordability was already gone.

5) How it impacts the “common person in the street

1. First-time buyers get locked out. With prices up and rates up, down payments are harder. 74 of 103 experts said housing will be less affordable in 2-3 years.

2. Renters face pressure. If buying power falls, more stay renting. Landlords with pricing power raise rents, further squeezing budgets.

3. Geography matters. In Phoenix, Austin, Raleigh, buying power loss was severe. In expensive cores, it changed little because affordability was already low.

4. Wealth gap widens. Existing owners with equity can outbid new entrants. Younger generations without family help struggle.

What helps: Government housing programs improve affordability. Longer mortgage terms, subsidies, or shared equity can restore purchasing power without price crashes.

6) How purchasing power can be used by civil servants globally

Civil servants often have stable income, pensions, and job security—lenders love that. But fixed salary scales mean inflation erodes real purchasing power unless housing is addressed. Here’s how to leverage it:

A. Use stability to access credit

1. Leverage low-risk profile: Banks view civil servants as low default risk. Use that for pre-approvals, lower rates, or longer terms to boost buying power.

2. Cooperatives & housing schemes: Many governments offer civil service housing loans at subsidized rates or payroll-deducted mortgages. Nigeria’s FMBN, India’s government quarters, and UK’s First Homes schemes are examples.

B. Beat inflation with real assets

1. Buy early, even small. Real estate is an inflation hedge because rents and replacement costs rise. A civil servant buying a 1-bed flat on mortgage locks in today’s price; salary rises with inflation, but mortgage stays fixed.

2. House hacking/rentvesting: Buy duplex, live in one unit, rent others. Tenants pay mortgage. Or buy investment property in cheaper city while renting near work. 43% of people <40 consider this vs. 9% of boomers.

C. Time rate cycles

1. Buy when rates peak, refinance when they fall. A 1% drop can restore 10%+ buying power. Civil servants can wait because job is secure, unlike commission workers.

2. Avoid “timing the market.” Prices may keep rising while you wait. If you need housing, buying power today may be better than tomorrow’s.

D. Use policy & benefits

1. Tax reliefs: Mortgage interest relief, though regressive, still exists in some countries. Use it.

2. Transfer below market value: In Canada and others, parents can transfer property to children below market to preserve family purchasing power.

3. Location arbitrage: Use postings to high-growth secondary cities. Purchasing power is higher where prices are lower but salary is national.

E. Build purchasing power outside salary

1. Side income for down payment: Agency, short-let management, or land services create cash to invest.

2. REITs/fractional ownership: Start with $10–₦50,000. Get real estate exposure without full mortgage. Builds equity for later purchase. 3. Land banking: Use stable income to buy titled land in growth corridors. Hold 5-7 years. Low maintenance, high appreciation.

7) Key points to remember

In conclusion

Purchasing power is the real governor of real estate. Prices can rise, but transactions only happen when buyers qualify. For investors, it signals when to buy, sell, or hold. Rising rates kill leveraged buying power but reward cash and equity. For the common person, it’s the difference between owning and renting forever.

For civil servants globally, stable income is your superpower. Use it to access credit, buy inflation-hedged assets, and leverage housing schemes. In a world where affordability is the casualty of rising prices, purchasing power is the shield. Build it, protect it, and deploy it before inflation eats it.

The market doesn’t care about your dreams. It cares about your DTI ratio. Make sure yours qualifies.